How synthetic data is shaping the insurance landscape

Data-centric sectors such as finance, healthcare, cybersecurity, and, of course, insurance have been navigating through stormy seas in recent years. The insurance sector, in particular, is struggling with an expanding data universe. At the same time, they’re fending off cyber threats and data breaches, resulting in tighter regulations around data collection, storage, and usage.

Understanding and using data has never been easier. But, paradoxically, regulations and software limitations hold back innovation in the insurance industry, making it hard to outperform competitors. Using production data is almost impossible due to privacy concerns and regulations. Creating mock data for testing purposes is time-consuming, expensive, and may not accurately represent the real world's diversity. Additionally, AI algorithms used in the insurance industry can be biased due to the lack of diverse data representation.

To overcome these challenges, insurance companies are exploring new solutions. One promising approach is the use of synthetic data. Synthetic data offers an innovative way to transform insurance practices by providing realistic data without compromising individual privacy.

In this blog post, we will explore the concept of synthetic data and its impact on the insurance industry. We will see how insurance companies use synthetic data to improve risk assessment, streamline claims processing, enhance fraud detection, and aid in software testing for insurance purposes. Additionally, we will discuss the ethical considerations surrounding synthetic data and how it helps insurance companies prepare for the future.

What is synthetic data, and why it matters in the world of insurance

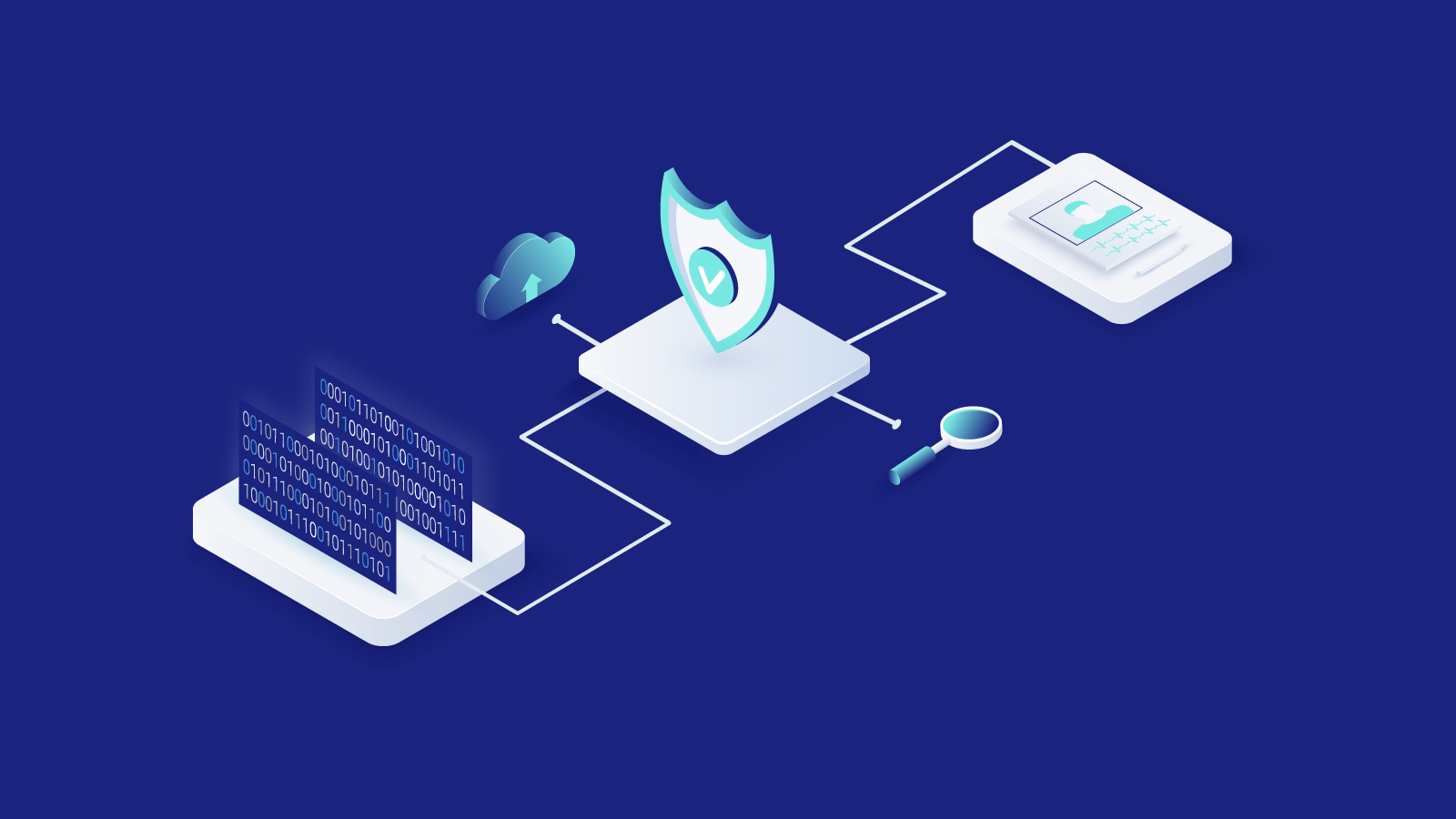

Synthetic data is the computer-generated simulation of real-world data. It has the same characteristics as production data but contains no personally identifiable information (PII). This makes it ideal for testing and training AI algorithms without jeopardizing individual privacy.

The adoption of synthetic data has been shaking up the insurance industry, and it's not difficult to see why. In the world of insurance, accuracy and detail are paramount, and traditional data collection methods for risk assessment and claims processing are often tedious and costly.

Additionally, real-world datasets commonly contain gaps in information that lead to inaccurate predictions or missing details that could significantly impact decision-making. Synthetic data offers a solution: it is generated with a high level of accuracy and is customizable to the specific needs of each application.

It is also a game-changer for risk modeling. It allows for the creation of countless scenarios, enabling companies to prepare for even the most unlikely events. In an industry where understanding and predicting risk is crucial, this is a significant step forward.

But perhaps the most appealing aspect of synthetic data in insurance is still its ability to safeguard privacy while providing valuable information. As regulations around privacy continue to tighten, synthetic data offers a compliant solution that doesn't sacrifice the quality of insights.

In a world of ever-increasing data regulations and the constant need for accuracy, synthetic data is a win-win solution. It offers an innovative way to access quality datasets without needing expensive data collection or relying on existing datasets that may be outdated, inaccurate, or privacy-compromising.

Use cases of synthetic data in the insurance sphere

Synthetic data offers endless possibilities for generating diverse and unique datasets, catering to a wide range of applications and scenarios. Let's take a look at how insurance companies make use of it.

Synthetic data in action: reinventing risk assessment

Risk assessment lies at the heart of the insurance industry, driving critical decisions that determine premiums, coverage, and overall business strategies. However, traditional risk assessment methods often fall short of capturing the complexities of the modern world.

This is where synthetic data steps in to improve risk assessment practices in the insurance sector. With its help, insurers create diverse datasets encompassing a wide range of scenarios.

Unlike conventional data collection, which is often limited by historical data or specific demographics, synthetic data is tailored to include various risk factors and demographic variables. This enables insurers to make more accurate risk predictions and better understand potential outcomes.

One of the significant advantages of synthetic data in risk assessment is its ability to account for extreme or rare events. In the real world, certain events may occur infrequently but have a significant impact when they do. With synthetic data, insurers simulate these rare occurrences and assess their potential consequences, allowing them to develop more robust risk models.

Moreover, it empowers insurers to analyze and address potential bias in their risk models. By ensuring diverse data representation, synthetic data helps reduce the risk of biased algorithms, leading to fairer and more inclusive risk assessments. This is crucial in an industry where biased algorithms could result in discriminatory practices and negatively impact customers from underrepresented groups.

Another key aspect of using synthetic data in risk assessment is the ability to explore various risk factors simultaneously. Insurers are able to experiment with different variables and combinations to identify the most influential factors affecting risk. This level of exploration allows them to fine-tune their risk models and make data-driven decisions that optimize their business outcomes.

Reshaping claims processing: the synthetic data advantage

Claims processing is another critical function for insurance companies, as it directly impacts customer satisfaction and overall operational efficiency. Traditionally, claims processing has been a labor-intensive and time-consuming process, often prone to errors and delays.

However, by using synthetic data, insurance businesses are gaining a significant advantage in streamlining claims processing and providing better support to their policyholders.

One of the key benefits of using synthetic data in claims processing is the ability to create realistic and diverse datasets that represent various types of claims. It allows insurers to simulate different scenarios, from routine claims to complex and rare events. This comprehensive dataset enables insurers to fine-tune their claims processing workflows, ensuring they are well-prepared to handle any claim that comes their way.

Additionally, it accelerates the claims processing timeline, leading to faster and more efficient service for policyholders. With access to high-quality synthetic data, insurers optimize their claims handling procedures, automating specific tasks, and reducing manual intervention. As a result, claims are processed more quickly and accurately, resulting in improved customer satisfaction and loyalty.

One of the critical challenges in claims processing is handling confidential and sensitive customer information securely. With real-world data, there is always a risk of breaches or privacy violations. However, synthetic data helps alleviate this concern as it is generated artificially, without containing actual customer records or sensitive details. This privacy protection ensures that customer data remains secure, compliant with regulations, and free from the risks associated with using actual production data.

The insurance industry has long sought to improve customer service and cut costs. With the help of synthetic data, insurers now do both without sacrificing accuracy or speed. By leveraging the power of artificial intelligence and machine learning, they are able to create more efficient claims processing systems tailored to their unique needs.

Detecting fraud deception with synthetic data

If anything results in substantial financial losses and damage to an insurer's reputation, it is fraud. Detecting and preventing fraud requires advanced techniques and robust algorithms, exactly what synthetic data provides.

It offers a unique advantage in fraud detection by allowing insurers to create realistic and diverse fraud scenarios. Fraudsters continuously evolve their tactics to evade detection, making it challenging for traditional fraud detection methods to keep up. Synthetic data enables insurers to simulate sophisticated fraud schemes, providing a comprehensive dataset for training and fine-tuning fraud detection algorithms.

One of the significant challenges in fraud detection is the lack of diverse data representation. Real-world datasets may not encompass all possible fraud patterns, leading to gaps in the training data that fraudsters can exploit. Synthetic data addresses this issue by generating data that spans a wide range of fraud scenarios, empowering insurers with a more comprehensive understanding of potential fraudulent activities.

By using it, insurers will enhance their fraud detection algorithms' accuracy and reduce false positives that occur when legitimate claims are flagged as potentially fraudulent, leading to delays and frustration for policyholders. With high-quality synthetic data, insurers refine their algorithms to identify genuine fraud signals more accurately, ensuring that legitimate claims are processed smoothly.

Another crucial advantage of using synthetic data for fraud detection goes back again to its ability to safeguard customer privacy. Fraud detection algorithms require access to sensitive data, making privacy protection a significant concern. Synthetic data provides a privacy-compliant solution by generating data containing no customer information, ensuring individual privacy is upheld throughout the fraud detection process.

Software testing with synthetic data

Using personal data in development and testing environments has become a significant concern, especially in light of stringent privacy regulations like GDPR, CPRA, and ISO 27001, including its newest version from 2022. In the past, developers often used real customer data to test new features and identify bugs. However, with more stringent privacy regulations, this leads to significant privacy risks.

Another issue worth mentioning when discussing software testing is the challenges associated with hiring and retaining technical talent. According to a 2023 Gartner survey of software engineering leaders, talent hiring, development, and retention are the top challenges they currently face.

This emphasizes the importance of improving test data management (TDM) practices to alleviate the burden on product teams and enhance software testing processes. Synthetic data offers a new approach to TDM, allowing insurance companies to avoid the challenges of utilizing production data for testing purposes.

One of the main advantages of synthetic data in software testing is its ability to create diverse and representative datasets. Production datasets may be large, containing confidential and private information, making them impractical for testing. Synthetic data, on the other hand, is tailor-made to include the necessary characteristics and features, making it a flexible and reliable testing resource.

Database engineering leaders integrate synthetic data generation into their testing processes, reducing the reliance on production data as the first stage of a TDM initiative. This change in perspective empowers developers and testers to access relevant data without compromising sensitive production information or going through complex data masking or pseudonymization procedures.

Finally, synthetic data mitigates the challenges associated with data relationships within and across production data models. Running applications on top of subsetted production data is problematic, but synthetic data removes these constraints, making the testing process more efficient and frictionless.

Investing in ongoing test data management is crucial for insurance companies to ensure continuous improvement in software testing practices. By incorporating TDM into the software development and testing disciplines, insurance companies will support product teams in their testing efforts and maintain their developers' and testers' enthusiasm and confidence.

Embracing inclusivity: combating bias with synthetic data

As data-driven decision-making becomes increasingly prevalent, the insurance industry is less of a stranger to discrimination. Exclusionary underwriting practices and bias in data-driven applications can lead to unfavorable outcomes for specific groups.

Bias in AI algorithms has far-reaching implications for insurers and their customers. From risk assessment to claims processing, biased algorithms lead to unfair treatment, resulting in higher premiums for certain customer groups and inadequate coverage for others. These biases not only tarnish the reputation of insurance companies but also affect the lives of policyholders.

Unlike real-world data, synthetic data is artificially generated with precision and tailored to include diverse demographics, ensuring fair and accurate representations of various customer groups. It allows insurers to simulate a wide range of scenarios, including those underrepresented in traditional datasets. By including these scenarios in training AI algorithms, insurers develop more robust models less prone to biased decision-making.

However, while synthetic data is a powerful tool in mitigating bias, it is essential to acknowledge that bias can also be introduced during the data generation process. Ensuring ethical and responsible data generation practices is paramount to avoid perpetuating existing biases or inadvertently creating new ones.

The ethical considerations of synthetic data in insurance

As insurers tap into synthetic data for decision-making, they must be mindful of the ethical implications. While it presents a great way to tackle various challenges in the insurance industry, with this technological advancement comes the duty to ensure responsible data usage and protect individual privacy.

As you've probably guessed, one of the primary ethical considerations of using synthetic data in insurance practices is data privacy. As insurers generate synthetic datasets to simulate real-world scenarios, they must be vigilant in safeguarding sensitive customer information and adopt stringent data governance practices to prevent potential data breaches or misuse of information.

The usage of synthetic data also raises questions regarding consent and transparency. Unlike traditional data, synthetic data is not obtained directly from individuals; hence, the issue of explicit consent is somewhat ambiguous. It's crucial to ensure that the generation and use of synthetic data respect the principles of informed consent, even though the data is not directly linked to any particular individual.

Do stakeholders, especially policyholders, have a right to know how their data is being used and processed? How can insurers ensure that the synthetic datasets they use represent their customers?

These are some of the questions that need to be asked and answered before deploying any synthetic data-driven solutions. After all, a lack of transparency could lead to mistrust and skepticism toward insurance companies, potentially undermining the credibility and acceptance of synthetic data technology in the long run.

Furthermore, ethical considerations extend beyond the use of synthetic data in risk assessment and claims processing. Insurers must also consider the impact of synthetic data on employees and stakeholders. Ensuring that employees are adequately trained in the responsible use of synthetic data and promoting a culture of ethical data practices are crucial steps in adopting this technology.

Lastly, the distribution of benefits from synthetic data is another ethical dimension that requires contemplation. Using synthetic data could lead to significant cost reductions for insurance companies. It is essential to consider how these savings are distributed. Are they used to lower premiums for policyholders? Or are they primarily benefiting the insurers' bottom line? These questions reflect the broader issue of equity and fairness in applying synthetic data.

Unlocking InsurTech's potential: Bridging the gap with synthetic data

The opportunities synthetic data presents to insurance companies go far beyond cost savings, improved accuracy, and data privacy. In fact, it has the potential to completely reshape the industry.

Driven by the rise of InsurTech startups, short for Insurance Technology, the sector is undergoing a digital transformation. New technologies alongside machine learning (ML) and the Internet of Things (IoT) are making it possible to create better customer experiences, more efficient operations, and faster claims processing.

However, most of these startups face the same obstacle: the lack of access to crucial data held by industry giants such as AXA, Zürich, and others, primarily due to stringent privacy regulations. And without this data, InsurTech startups are hindered from fully testing and realizing their ideas and technologies.

This is where synthetic data emerges as the crucial bridge between the aspirations of InsurTech startups and the data they need to thrive. With it, InsurTech companies can now access the data they need to develop and test their products without compromising customer privacy. As a result, the insurance sector has experienced a surge in new ideas and technologies that are transforming the industry from its core.

This bridges the gap between ambitious startups and established giants, fostering an environment of healthy competition, rapid innovation, and, ultimately, better offerings for customers.

Conclusion

The insurance industry has only begun to scratch the surface when it comes to exploiting the potential of synthetic data. As data-driven decision-making becomes increasingly critical, insurance companies face challenges in collecting, managing, and utilizing data responsibly.

However, this is also an opportunity to leverage technology for improved efficiency and better customer experiences. By taking the necessary measures to create high-quality datasets, insurers reap the many benefits of synthetic data while ensuring compliance with regulations. With technological advances and rapidly changing customer demands, synthetic data promises a bright future for insurance companies.

So far, we have seen how synthetic data detects fraud, predicts risk, reduces costs, develops personalized products, and stays ahead of the competition. As businesses become more data-driven, we expect the use of synthetic data in the insurance sector to continue to rise. The possibilities are endless, and we look forward to seeing what other innovative applications for synthetic data we will come up with in the future!